|

Industry News: Global Personal Care Market Report 2023

Report catalog

Chapter 1:A rapidly changing global market

1. The overall growth of the online market is weak 2. Global economic pressure

Chapter 2:The analysis of regional market changes

1. Asia: The Chinese market has become an important consumer position 2. the United States: online market share will reach 1/3 3. Europe: Germany becomes a bigger consumer market 4. the United Kingdom: market expansion was hindered, Black Five preheating in advance

Chapter 3:Consumer behavior insight

Chapter 4:Deconstruct the influence of social media channels

1. The rise of artificial intelligence 2. Mobile APP becomes an anchor for user retention 3. The rise of the concept of virtual stores and meta-universe shopping 4. The traditional e-commerce platform is still "Sweet pastry"

In recent years, the size of the personal care market has grown by an average of 4% to 5% per year. In 2020, during the outbreak of the pandemic, the market growth was slightly "cooled" due to people facing travel restrictions. As more people join the middle class, more consumers are turning to non-essentials such as personal care products. L 'Oreal forecasts that the global middle class will grow by 800 million people by 2030.

Chapter 1:A rapidly changing global market 1. The overall growth of the online market is weak In the personal protection market, about 30% of sales come from online channels, and the return of consumers to offline channels in 2022 has not had a major impact on the revenue of this channel. In 2019, the online sales of personal care products accounted for 22%. In 2022, that number dropped to 31% from a peak of 33% in 2021.

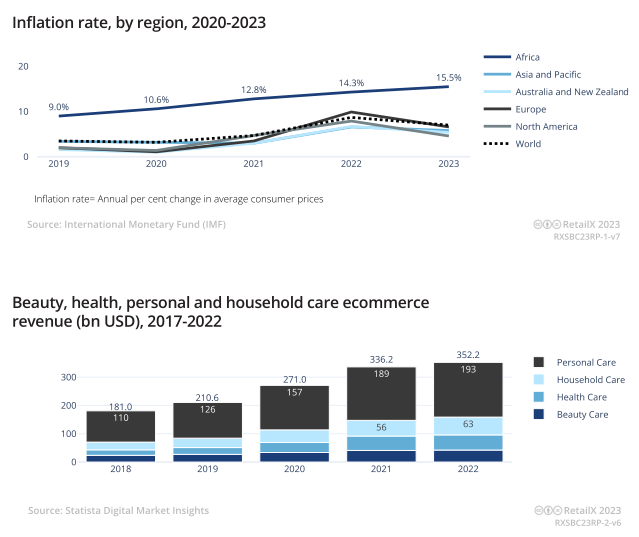

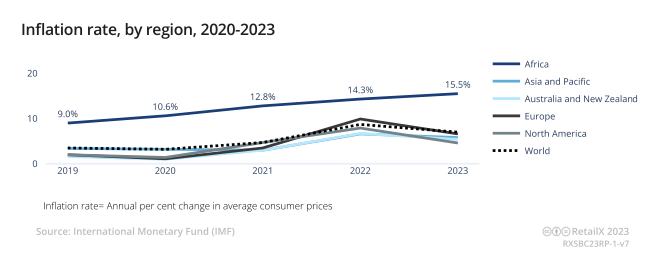

2. Global economic pressure The inflation and cost of living crisis has raised consumer concerns, with energy and food prices rising throughout 2022, reducing the level of disposable income for the population. Some regions and individual countries have been hit harder. For example, Africa continues to have the highest inflation rate, with the country's inflation rate continuing to rise to 15.5% in 2023. Zimbabwe, for example, has an inflation rate of almost 100 percent.

Chapter 2:The analysis of regional market changes 1. Asia: The Chinese market has become an important consumer position As an important consumer market of personal care products, the influence of Asia cannot be ignored. The region also needs to be uniquely positioned, with consumers looking for a different shopping experience than in other regions. As a more active consumer group in the region, Generation Z consumers are actively seeking fresh shopping experiences and novel products. In addition, 90 percent of Gen Z consumers surveyed said that sustainability is an important consideration when purchasing personal care products. In recent years, Western brands have been the first choice of consumers and are also seen as more trustworthy or better quality, while Chinese brands have become a rising "different army" and are launching an onslaught against Gen Z consumers. Many consumers prefer to pay by installments rather than cash. At the same time, Chinese millennials are also the main consumer group of personal care in China. According to Daxue Consulting, the age group accounts for 31% of sales in the personal care category. As in other countries, Chinese consumers have turned to online shopping during the pandemic. L 'Oreal said that China is a challenging market, and its luxury category business growth slowed sharply in the Chinese market in 2022, according to the group's full-year financial results show that its consumer goods business accelerated the pace of market share growth in the fourth quarter, and the group's online sales also achieved double-digit growth. Overall, consumer spending on personal care products in China will reach $80 billion in 2021, up 10% from 2020. It is predicted that by 2027, the average annual growth rate of China's personal care market will be more than 5%. Among them, the sales growth rate of men's personal care category exceeds the global average. In 2021, the sales of China's male personal care market will reach $1.44 billion. 2. the United States: online market share will reach 1/3 The United States is one of the major markets for care products, with sales reaching more than $87 billion in 2022. By comparison, sales in China reached $55.3 billion. The difference between the two countries is the level of online sales, with China outpacing the US in both digital channel sales and mobile device sales. Mobile commerce accounts for 49% of online sales in the Americas and up to 80% in Asia. In the United States, online sales of personal care in 2022 reached $11.7 billion, and online sales in 2021 reached $10.54 billion, highlighting to some extent the decline in consumer demand for online shopping after the end of the epidemic. It is expected that by 2026, the online market size of personal care in the United States will grow slowly at an average annual rate of 1%. CoreSight Research predicts that a third of the U.S. market will be online. Amazon Prime Day membership Day is an important promotion of the US personal protection market. Laneige, for example, became one of the top-selling beauty and personal care brands in the United States on Amazon's Prime Day 2022, a move the company called "a new milestone." The brand's lip masks, lip glazes and lipsticks are all bestsellers.

In addition, according to Future Market Insights, U.S. consumers will spend more on luxury cosmetics in the decade leading up to 2033, making the region the world's leading luxury cosmetics market. Skincare market share will maintain the largest share of global luxury beauty consumption. 3. Europe: Germany becomes a bigger consumer market Germany, France and the United Kingdom are the top three European personal care markets, with consumers spending an average of about $60 per year on this category. The UK has a larger proportion of online shoppers than any other major European market. 30% of UK online shoppers buy personal care products. That compares with 26 per cent in Germany. In terms of revenue alone, however, Germany is a much bigger market. Overall, 35% of online consumers in the European market have purchased personal care products, and 47% of these consumers have purchased through mobile channels rather than desktop channels. The majority of the European personal care market is still held by Amazon, and Sephora has a major market share among professional beauty care retailers. Douglas and Boots are equally prominent as major retailers in this segment. Three countries, Spain, the United Kingdom and Norway, have become the "battleground" of the European market. China's Alibaba chose Spain as the first location in Europe to launch its Tmall e-commerce platform, while Sephora is making a full push into the UK following its acquisition of Ferrer. According to Alibaba Group President Michael Evans, Tmall launched a pilot project in Spain in June 2023, and will expand across the European market in the future. Tmall's luxury pavilions have been a key entry point for marketing and product launches. In a talk at VivaTech Paris, Evans said Tmall's strategy in Europe will be to serve local brands and local consumers in local markets. This means that Tmall is entering a highly competitive market, especially in the area of beauty care retailers. 4. the United Kingdom: market expansion was hindered, black Five preheating in advance According to the UK e-commerce association IMRG, online sales of personal care in the UK grew by nearly 40% in 2020, but fell by 10.7% in 2022, with market expansion hampered not only by people returning to physical stores after the pandemic, but also by supply chain and inflation issues posing other challenges for retailers. Market jitters over intermittent postal strikes and retailers' ability to deliver online orders around the 2022 Christmas shopping season are also challenging factors for UK online retailers. In addition, retailers launched Black Friday sales in the UK as a whole long before other categories of retailer sales. Overall, online revenue in the care category fell in the UK market in 2022, but still increased during Black Friday, and online sales of makeup products also increased significantly during the festive period. Sales in the high-end beauty and cosmetics category also rose sharply in early November.

Chapter 3:Consumer behavior insight Retailers in the mass market try to gain a larger market share through marketing measures such as membership subscription services, multiple discounts on purchases of the same product, and repeat purchases. While consumers may be loyal to a brand or product they love, such as skincare, there are many other more easily swayed consumers who are more willing to buy new products and try other brands.

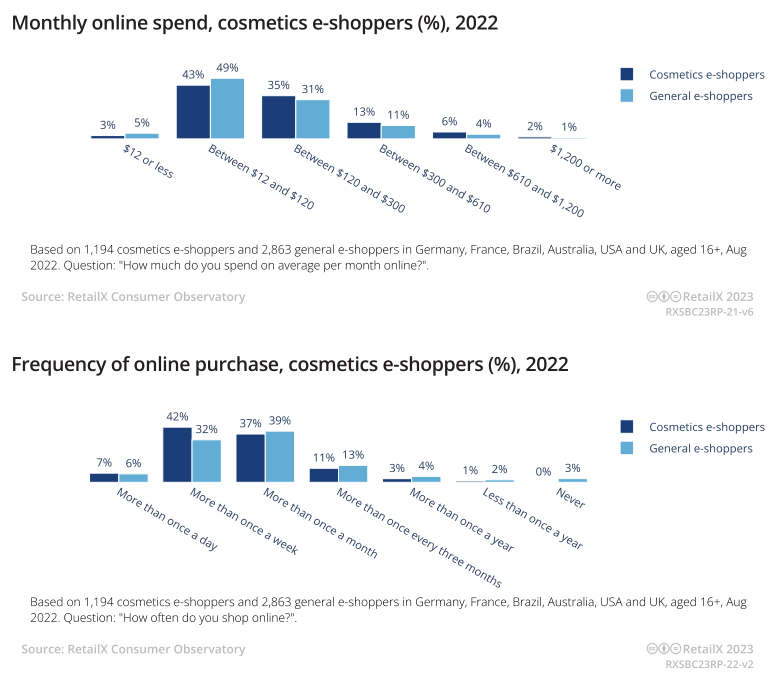

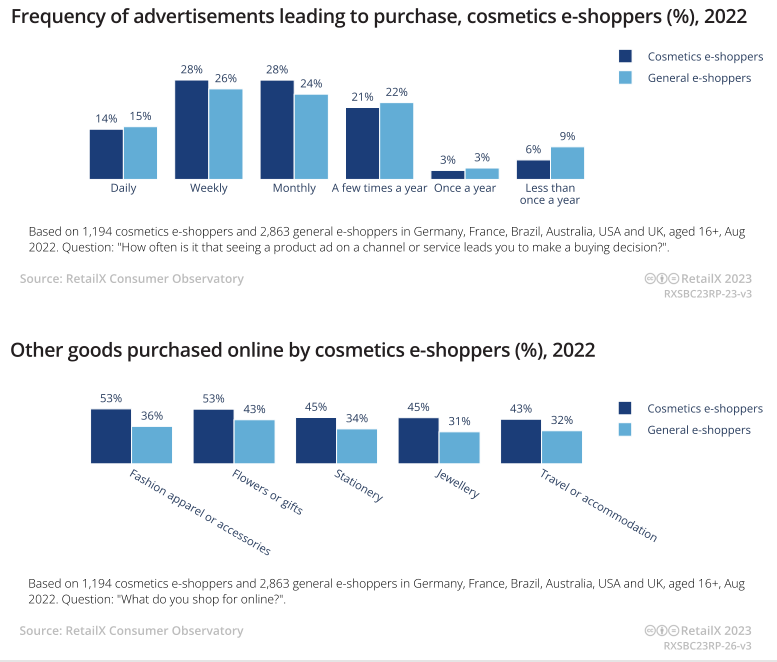

42% of online consumers in the personal care category shop online more than once a week, while 32% of online shoppers only buy products in other categories. 13% of general online shoppers shop online more than once every three months, compared to 11% of personal care online consumers. According to the results of a survey conducted by RetailX in multiple countries, the majority of online consumers in the consumer care category are under the age of 34. Young people who have grown up with the Internet and e-commerce also tend to be less loyal to brands, which also makes them more likely to click on targeted ads. These people also tend to want to know more about the products they are buying, learn about the ingredients and benefits of products, and be more price sensitive in the current economic climate.

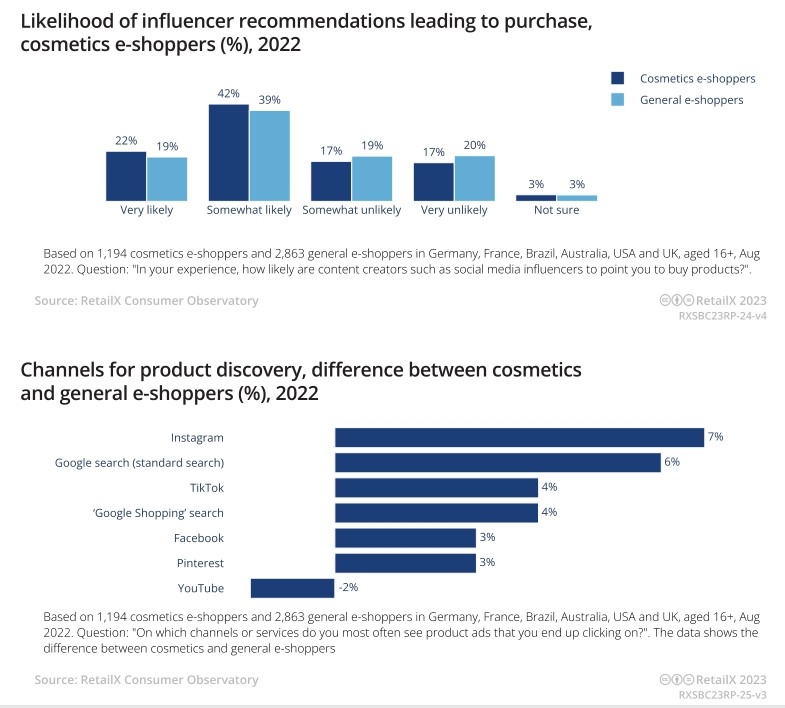

Chapter 4:Deconstruct the influence of social media channels The role of social media is crucial for the personal care industry. The reach of platforms such as Instagram and TikTok allows brands and retailers to engage directly with consumers. Both Kols and content creators play an important role in marketing campaigns, and consumers turn to them for expertise and advice. According to a survey by RetailX of consumers in several countries, 22 percent of online shoppers are "very likely" to buy a product after seeing a recommendation from an influencer, while another 42 percent are "somewhat likely." In addition, 20% of ordinary online consumers said they were "very unlikely" to buy products recommended by celebrity bloggers.

Overall, personal care buyers in France are less likely to place an order based on the advice of influencer bloggers, although nearly 50% of respondents are likely to be influenced to some extent by influencers. In the United States and Australia, the biggest differences between consumers are those who buy personal care online and those who do not. In the United States, there is a 15 percentage point gap between the two groups, while in Australia, personal care consumers are 13 percent more likely to buy that category on social media channels than other categories. Consumers in Brazil are the most likely to be influenced to buy by social media content creators. 38% of Brazilian online consumers said they would be willing to buy products recommended by bloggers, while 43% said they would "probably" take action. Trust in social media bloggers is particularly high in South American countries, where 80 percent of online shoppers are. Instagram is the main social media channel where consumers see and click on ads most often, especially in Brazil.

1. The rise of artificial intelligence The application of artificial intelligence (AI) in e-commerce is gradually gaining popularity. More compelling for consumers is the use of augmented reality virtual fitting and skin analysis tools. These tools have become so ingrained in the industry that consumers are used to visiting websites, mobile apps or physical stores to get personalized recommendations for skincare products. The skincare analytics tool uses questions answered by users, images from the consumer's webcam or phone camera, and artificial intelligence technology to analyze skin areas, identify skin types, and the ingredients best suited to allay consumer concerns. Tools such as these help provide consumers with a personalized experience, increased warranty on the items they purchase, as well as increased shopping engagement and reduced product returns. Since launching the AI skin Analyzer, Marianna Naturals has seen a 300% increase in time spent on its website and a 30% increase in website sales. In contrast, the Estee Lauder Company has developed an app that uses AI and augmented reality technology to give visually impaired consumers a greater sense of engagement when applying makeup. Once the makeup is done, the app analyzes the user's facial examination to make sure all the application is correct and even. The app describes where lipstick, eyeshadow or foundation needs to be embellished, and even gives advice. Since ChatGPT can be integrated into websites and mobile applications, merchants can use knowledge about brands and their product catalogs, as well as macro information about beauty and personal care, to understand and answer complex or delicate consumer questions in real time. What's more, ChatGPT uses natural language, so consumers can ask questions naturally and receive responses in the same way, without language restrictions. 2. Mobile APP becomes an anchor for user retention In addition, many retailers will develop a mobile APP to attract consumers and guide purchases, but also through the mobile app to provide tutorials, incentives and rewards for new and existing customers, video tutorials to combine the expertise of makeup artists with AI-powered skin analyzer to personalize the experience and AR virtual makeup test. Help users find their perfect product fit, and allow shoppers to access out-of-stock or newly released products first, all supported by loyalty programs, rewards, and member gifts. 3. The rise of the concept of virtual stores and meta-universe shopping Other brands in the beauty industry are launching virtual experiences to raise awareness of products among potential new customers. Many of them are temporary pop-up stores. South Korean skincare brand Laneige is one of the latest brands to launch in the virtual beauty space, with its virtual store enabling visitors to explore the brand through digital entertainment, video quizzes and explanations of key product ingredients. Visitors can add items to their basket in the store and buy directly from the brand. Obsess, the technology company behind Laneige's virtual store, found that visitors to a global consumer goods brand spend 10 times more time in a virtual store than on the brand's traditional e-commerce site, while visitors are 112% more likely to make a purchase at a leading luxury brand store. Shiseido has moved into virtual stores and virtual worlds. The Japanese company has found that consumers are more willing to interact with brands in such an environment than on traditional social platforms. Shiseido's Nars Color Quest, launched on gaming platform Roblox, attracted 41.9 million visitors between July and October 2022. The game itself uses different islands corresponding to makeup colors with non-player characters, which players can interact with to unlock special abilities. Players can also earn microbadges and use virtual currency to purchase goods and virtual appearances. 4. The traditional e-commerce platform is still "Sweet pastry" In the personal care industry, marketplaces such as Amazon attract higher levels of traffic than brands and retailers' own e-commerce sites. Even multi-category retail platforms capture more traffic than dedicated vertical personal care platforms. In addition, retailers in the beauty and personal care industry are opening up opportunities in the market as a business model that allows them to reduce expansion risks. Selected brands can sell products on niche retail websites and fulfill orders directly to consumers without the retailer having to hold inventory in a warehouse or store. For retailers who have become leaders in the beauty care industry, the extension of this channel through e-commerce platforms provides relatively risk-free, low-cost performance growth. If a retailer already stocks 70% of a brand's inventory, it can sell through an e-commerce platform outside of their official website. Profits are also higher than traditional retail models, because the responsibility and burden of pricing fulfillment, content creation, and so on belongs to the brand rather than the retailer itself. |

|

LinkedIn:Personal Care Expo (PCE) LinkedIn:Personal Care Expo (PCE) Ins:yinghezhanlan Ins:yinghezhanlan Facebook:Pce Yinghe Exhibition Facebook:Pce Yinghe ExhibitionPrivacy policy 沪ICP备17037700号 |